Learning objectives :

After studing this chapter, students shall be able to :

- Exaplain the concept of Bill of Exchange and Promissory Note.

- Distinction between Bill of Exchange and Promissory Note.

- Define Important terms of Bill of Exchange and Promissory Note.

- Record the Accounting Treatment of Bill of Exchange under different Circumstances

Suggested Methodlogy :

Illustration - cum - Explanation method.

A Bill of Exchange and Promissory Note both are legal Instruments which facilitate the credit sale of goods by assuring the seller that the amount will be recovered after a certain period. Both of these are legal instruments under the Negotiable Instruments Act, 1881.

BILL OF EXCHANGE

"A Bill of Exchange is an instrument in writing containing an unconditional order signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument." Section 5 of the Negatibale Instrument Act, 1881

Features of a Bill of Exchange are :

- A Bill of Exchange must be in writing.

- It must contain an order (and not a request) to make payment.

- The order of payment must be unconditional .

- The amount of bill of exchange must be certain.

- The date of payment should be certain.

- It must be signed by the drawer of the bill.

- It must be accepted by the drawee by signing on it.

- The amount specified in the bill of exchange is payable either on demand or on the expiry of a fixed period.

- The amount specified in the bill is payable either to a certain person or to his order or to the bearer of the bill.

- It must be stamped as per legal requirements.

PARTIES TO A BILL OF EXCHANGE

1. DRAWER :

Drawer is the person who makes or writes the bill of exchange. Drawer is a person who has granted credit to the person on whom the bill of exchange is drawn. The drawer is entitled to receive money from the drawee (acceptor).

2. DRAWEE :

Drawee is the person on whom the bill of exchange is drawn for acceptance. Drawee is the person to whom credit has been granted by the drawer. The drawee is liable to pay money to the creditor/drawer.

3. PAYEE :

Payee is the person who receives the payment from the drawee. Usually the drawer and the payee are the same person. In the following cases. drawer and payee are two different persons :

(i) When the bill is discounted by the drawer from his bank- payee is thebank.

(ii) When the bill is endorsed by the drawer to his creditors : payee is the endorsee.

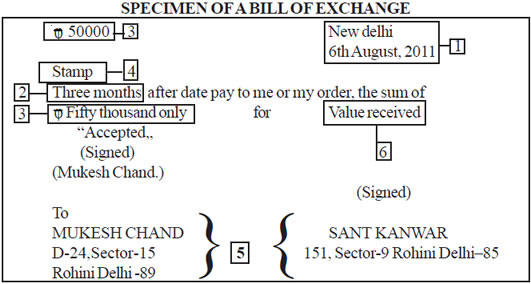

CONTENTS OF BILL EXCHANGE :

1. DATE - The date on which a bill is drawn, is written on the top right corner of the bill. It helps in determining the date of maturity of the bill.

2. Term/Tenure - Term specifies the time period for which a bill is written. It should be specified in the body of the bill.

3. Amount - Amount in figure should be mentioned in the top lelf corner and amount in words should be mentioned in body of the bill.

4. Stamp - Stamp of proper value depending upon the amount of bill must be affixed on the bills of exchange.

5. Name of parties - The name and addresses of the drawer and the drawee should be mentioned in the bill of exchange.

6. For Value Received – It means the bill has been issued in exchange of some consideration. These words are very important because law does not consider those agreements which have been made without consideration.

CBSE Accountancy Class XI ( By Mr. Aniruddh Maheshwari )

Email Id : [email protected]