6. Life Membership : Life membership is the fee received from those members who do not pay periodic fee or subscription but pay a lump sum amount to become life time members.

(i) These members are generally permanent members.

(ii) Life membership fees can be added to capital fund or separately on the liabilities side of Balance Sheet.

7. Endowment Funds :

1. This fund is created from the bequest, legacy or gifts received by the Not-for-Profit organization. These funds are invested out- side.

2. The income from the investment of such funds is used for some specific purposes only.

3. Endowment funds shall be shown on the liabilities side of the balance sheet of Not-for-Profit organization.

Example :

An amount of `5,00,000 is received as Donation with condition that this amount will be invested as Fixed Deposit in a Bank. Income from this Investment will be used to distribute prizes to meritorius students of the society.

8. Honorarium : Honorarium is an amount paid to a person (other than employee) for rendering some special services for Not-for-Profit organization. It is treated as an expense fo Not-for Profit organization.

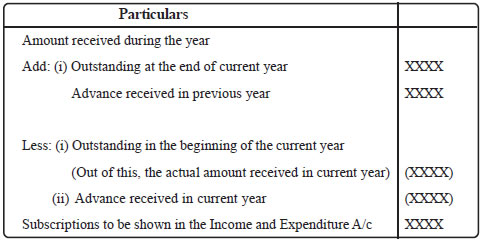

Calculation of Subscriptions to be shown in the Income and Expenditure Account for current year

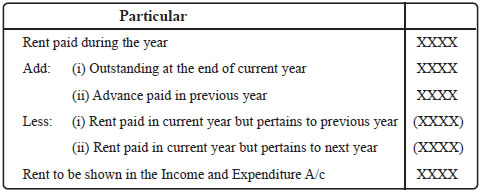

Calculation of Rent (An Expense) to be shown in expenditure side of Income and Expenditure

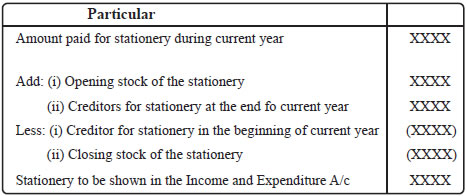

Calculation of Stationery (A consumable item) to be shown in Income and Expenditure Account

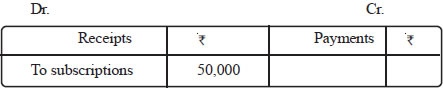

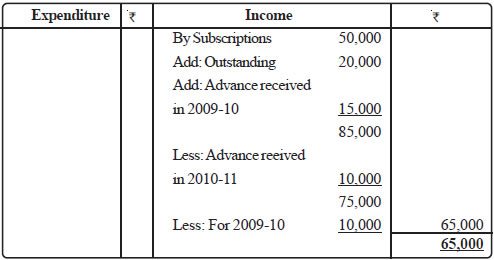

Illustration 1

From the following extracts of the Receipt and Payments Account and the additional information, you are required to compute the income from subscriptions for the year ended March 31, 2011 and show it in the Income and Expenditure Account for the year ended on March 31, 2011:

Receipts and Payments Account for the year ended on March 31, 2011

March 31, 2010 Rs. March 31, 2011 Rs. Subscriptions outstanding 10,000 20,000 Subscriptions received in advance 15,000 10,000

Solution :

Income and Expenditure Account. for the year ended on March 31, 2011

Importance Point :

Subscription for the current year only is shown in Income and Expenditure

Account for the same year, whether received or not.

CBSE Accountancy Class XI ( By Mr. Aniruddh Maheshwari )

Email Id : [email protected]