Errors Affecting Trial Balance.

Shown by star in the table showing

Errors : Types and Examples.(1) Errors in totalling of Subsidiary books or ledger A/cs - i.e. overcast or undercast.

(2) Error in the Balancing of Ledger A/cs.

(3) Error in posting to the correct A/c but with the wrong amount or to the wrong side or both.

(4) Errors of Paitial ommission

(5) Omitting to show an A/c in the Trial Balance.

RECTIFICATION OF ERRORS

When th errors are detected, these have to be rectified in the books of accounts. Rectification of errors depends upon :

- The type of error and

- The time of depiction of an error.

Time of Depiciation of an error means

- Errors detected before the preparation of Trial Balance.

- Errors detected after prepairing Trial Balance but before preparing final Accounts.

- Error detected after preparing Final Accounts.

Rectification of Errors detected after preparing Final Accounts is not in the syllabus. Hence we will discuss only type (i) and (ii)

I RECTIFICATION OF TWO SIDED ERRORS

Two sided errors are those errors which affect two sides of Accounts. These errors don't affect Trial Balance as discussed earlier.

These Errors are rectified by passing a Journal entry irrespective of the time of deficiation. In other words their rectifying entry will be same whether (a) the error is depicted before preparing Trial Balance or (b) after the preparation of Trial Balance but before the Final A/cs are prepared.

Steps for Rectification

(1) Locate the Effect of Error on Different Accounts

(2) The Account Showing Excess credit should be Debited.

(3) The Account Showing Excess Debit should be Credited.

(4) The Account Showing short Debit should be Debited.

(5) The Account Showing short Credit should be Credited.EXAMPLES (with Explanation)

(I) when an account has wrongly been debited in place of another A/c.

Recification will be done by debiting the correct account and Crediting the A/c which was wrongly debited.

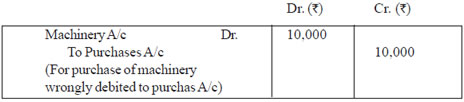

Example : Machinery purchased for Rs. 10,000 has been debited to Purchases A/c

Solution : Here two A/cs are affected

1- Machinery A/c is not debited its debit side is short by Rs. 10,000, where as purchases A/c is debited by mislake purchases A/c debit side is in excess by Rs. 10,000. While rectifying this mistake machinery A/c will be debited by Rs. 10,000

2- because it w as not debited earlier and purchases A/c will be credited be cause it was wrongly debited Hence.

Rectifying Entry is :

(II) When an account has wrongly been Credited in place of another account.

Example : Rs. 5,000 received from the sale of old furniture has been Credited to Sales A/c.Solution : This errors also affects the two A/cs

- Furniture A/c is not Credited its credit side is short by Rs. 5,000.

- Sales A/c is credited by mistake its credit side is in excess or Rs. 5,000.

- Therefore for rectifying this mistake Sales A/c will be debited because it was arongly Credited and Furniture A/c which was not Credited earlier will now be credited by Rs. 5,000.

Hence Rectifying entry is :

CBSE Accountancy Class XI ( By Mr. Aniruddh Maheshwari )

Email Id : [email protected]